What Buyers Need to Know

Watch the full webinar recording to hear directly from our experts and gain insights into the latest carbon market trends for 2026 - and what they mean for your business.

As climate ambition accelerates globally, the carbon market enters 2026 with renewed momentum. Integrity standards are rising, supply is evolving, and new policies are formalizing the role of carbon credits in corporate net‑zero strategies.

Our latest Carbon Market Outlook webinar unpacks these dynamics, helping companies understand how to stay ahead of tightening supply, rising quality expectations, and expanding opportunities for high-impact climate action.

Explore the key themes shaping the market below and hear from our experts in our on-demand webinar.

Watch the full webinar recording to hear directly from our experts and gain insights into the latest carbon market trends for 2026 - and what they mean for your business.

2025 saw carbon credit retirements grow by 9% compared to 2024. While headline retirements (211 million tonnes across 16 standards) remained slightly below the 2021–2023 peak, the underlying signals point to a maturing market, not one that is contracting.

Overall, 2025 revealed a market increasingly driven by integrity, transparency, and long‑term climate strategy alignment.

The developments of 2025 set the stage for significant evolution in 2026. Several trends point toward rising demand and increasing competition for high‑quality supply.

2026 will see continued expansion of the ICVCM’s Core Carbon Principles (CCPs). In 2025, CCP‑tagged retirements more than doubled, rising from 3% to 7% of total retirements, driven largely by Sustainable Infrastructure projects. As more CCP tagged credits come to the market - including IFM, REDD+, ARR, biochar and clean cooking – CCP availability is expected to grow, as will demand.

Independent ratings also continued to shape procurement decisions. Credits rated BBB and above increased their share of retirements, climbing from 28% to 34% of rated credit volume. This shift underscores the market’s increasing prioritization of quality, measurability, and robust governance.

CCP labels and independent ratings are becoming powerful quality markers in the market - helping set clearer expectations, raising the bar for integrity, and providing companies with a consistent first filter for identifying credible supply. As these frameworks expand in 2026, they will continue to play a central role in shaping what “good” looks like across methodologies, governance, and project design.

But labels and ratings alone cannot determine true project integrity. Deeper insight comes from understanding what is happening on the ground, and this is where bespoke technical due diligence (DD) remains indispensable to interrogate governance structures, methodology implementation, community outcomes, monitoring rigor, and long‑term performance.

With issuance continuing to decline in 2025, the VCM is now closer than ever to annual retirements outpacing annual issuance - a tipping point already reached within higher‑rated subsets like BBB+ and above where retirements have exceeded issuances every year since 2022. The stock of credits rated A or higher has fallen from around 90 million tonnes to under 75 million tonnes between 2022 and 2025.

This tightening will drive:

As the pool of high‑integrity supply narrows, companies are increasingly moving to secure future volumes early, particularly for removals and nature‑based solutions. Those buyers who act early will secure better access to quality supply.

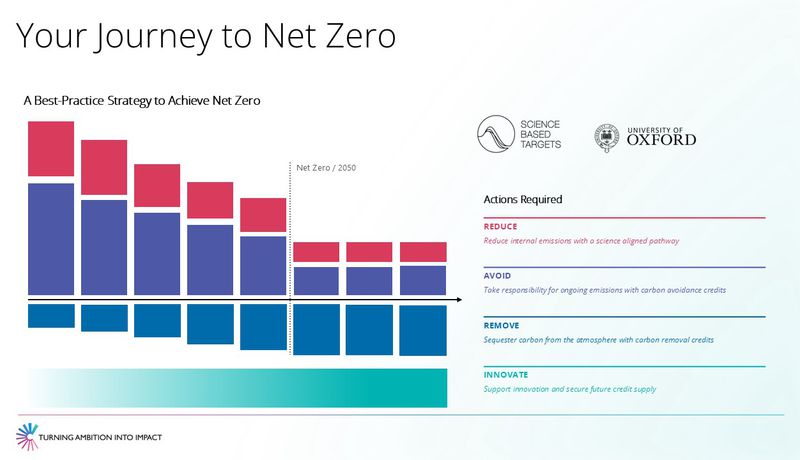

SBTi’s upcoming SBTi’s Net Zero Standard V2 introduces the “Ongoing Emissions Responsibility” framework- the first structured mechanism for recognizing carbon credits within corporate net‑zero strategies. Replacing “beyond value chain mitigation,” it marks a major shift - credits are now a defined component of the pathway to net zero, not optional extras.

The OER framework offers two tiers for companies taking responsibility for ongoing emissions (those not yet abated on the journey to net zero):

Recognized Status

Leadership Status

How credits fit into the framework

Carbon credits are recognized as eligible mitigation activities under both tiers. Companies can purchase credits from projects that avoid emissions (pre 2035) or remove CO₂ from the atmosphere. This creates:

In essence, SBTi v2 clarifies and formalizes the role of carbon credits in corporate climate strategies, reinforcing the need for high‑integrity supply, strong governance frameworks, and long‑term procurement planning.

Climate Impact Partners brings nearly three decades of technical expertise, working with climate leading organizations and a global network of more than 600 projects, offering:

Our 2026 recommended portfolio spans multiple technologies and continents, offering a strong foundation for any corporate looking to build a resilient, future‑proof climate strategy: Get in touch with our global experts.

Integrity is now the defining force in the voluntary carbon market and rather than slowing the market, it is accelerating demand for high‑quality supply. As supply tightens, prices diverge, and frameworks like SBTi formalise the role of mitigation outcomes, the VCM is entering a new era of disciplined, strategic growth.

Companies that act early - securing high‑integrity supply, entering long‑term offtakes, and leveraging robust due diligence - will be best positioned to lead in 2026 and beyond.