There is a lot of talk about growth in the carbon markets, but what does the research say, and what does this mean for the projects around the world that are delivering the emission reductions we so desperately need? Dan Thompson, Director of Global Sourcing explains.

Corporate Demand

Corporate demand for carbon credits has increased significantly in the past two years .

In 2021 the annual value of the Voluntary Carbon Market (VCM) exceeded $1billion for the first time,1 and in 2022 it saw a 30% increase in size, reaching an estimated value of $1.3 billion2

However, there are signs that the rate of growth is slowing, with the volume of carbon credits retired through the Gold Standard and Verified Carbon Standard (Verra) remaining stable in 2021 and 20223.

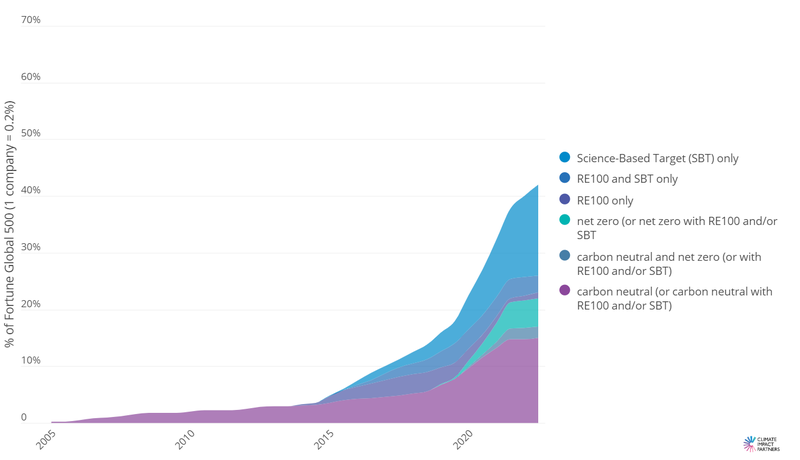

It is likely that large volume purchases by investors - enticed by rapid market growth – contributed to market escalation, which is now tailing off. Despite this, corporate demand remains and continues steady growth. Our recent Fortune Global 500 research, which tracks the climate commitments made by the world’s biggest companies, continues to show growth in corporate climate action: 42% of companies in the Fortune Global 500 have now delivered a significant climate milestone, or are publicly committed to do so by 2030, up from 11% last year4.

And while this increase in corporates taking responsibility for climate action over the past two years continues to drive demand, there is still room for growth.

Over 50% of the Fortune Global 500 companies still haven’t made commitments3. And they face increasing pressure from their stakeholders to act. Customers, investors, and staff all want to see business doing more.

Date of Fortune Global 500 companies’ public commitment that they are, or will be by 2030: carbon neutral, meeting an RE100, Science Based Target or net zero target. (Source: 2022 Fortune Global 500 Report)

The Taskforce for Scaling the Voluntary Carbon Market, which was established by the private sector to help the market meet the goals of the Paris Agreement, states that the voluntary carbon market must scale at least 15-fold by 2030 in order to play its part in the delivery of global climate targets.

Statements like this are leading to increased interest in scaling up existing emission reduction projects as well as attracting finance to develop new ones. But in order to deliver long-term success, projects need an informed approach to accessing the finance.

If you want to start or scale an emissions reduction project, how can you best capitalise on this potential new source of carbon finance to ensure you maximise project income and secure the sustainability of your project?

Complexity is Increasing

Working with over 500 corporate clients across six continents, we see first-hand the trends in the marketplace as they unfold. Companies are at vastly different stages in their climate journey, with a wide range of pledges and varying objectives in the decision to finance external emission reduction projects.

Best practice and corporate climate leadership is changing

As a result, corporates are seeking advice to make robust pledges and delivery plans, working with trusted partners who can help them deliver a strategy over the long term.

The majority look for a portfolio of projects that can generate high integrity emissions reductions and to ensure the climate claims they make are credible, accurate and in line with best practice – and to supply them with the materials that will support their action.

Managing their reputation while on the journey to decarbonise is becoming increasingly important as the media spotlight shines more brightly on anything that could be misleading.

We’ve worked with many clients for more than 10 years and are supporting them as they raise their ambition over the next decade. They rely on us to provide them with independent assurance about a project’s quality, integrity, and impact. And we conduct robust quality assurance on their behalf, giving them the confidence to invest.

Bondhu Chula Cookstoves Project, Bangladesh

Portfolio approach

Each company has its own priorities for the types of projects and the locations in which they want to take action, with many supporting a portfolio of projects in technologies and locations which fit their specific requirements. A portfolio approach enables corporates to manage risk, deliver to budget and support different regions relevant to their business.

This makes it more difficult for an individual project developer to access this demand, and more attractive to work with a partner who has already nurtured and understood these client relationships and which has established the systems and processes to meet and respond to client expectations.

Positive impact for people and biodiversity is key

Alongside verified emissions reductions, additional project impacts, generally those aligned with the UN Sustainable Development Goals (SDGs), continue to be strong motivating factors for corporates.

A focus on the positive social, biodiversity and equality impacts provided by our project partners is vital in attracting companies to purchase carbon credits or invest in project development.

That is why we choose to work with on-the-ground project implementation partners who understand the local stakeholders and ecosystems and have the highest standards of conduct. We also help quantify these multiple outcomes for corporates by taking projects through certifications like the Climate, Community and Biodiversity Standard (CCB), SD VISta and Gold Standard for the Global Goals and Plan Vivo.

Custom project development

Increase in demand has driven the price of carbon credits up to a level that makes new project development financially viable and we are seeing greater interest from our clients in financing new projects.

This represents a different level of engagement with projects over a much longer period, and with a different risk profile. Clients are highly selective in the partners with whom they work – and our project partners are equally selective in choosing funding partners who understand the real complexity of project development.

In the past 12 months alone, we have secured over $67.8m of funding to finance the early-stage development of new reforestation, forest restoration, and energy efficiency projects. And we are on track with our plan for that fund to grow significantly to protect and restore nature and improve livelihoods over the next five years.

Demand is for a mix of nature-based solutions, carbon reduction and carbon removal projects

There is an increased focus on biodiversity and in organisations pledging to reach net zero. As a result, nature-based projects (which both protect remaining forests and create new natural carbon sinks) will continue to be in demand.

However, our clients understand that all project types remain an important part of the set of solutions needed to reach our climate goals. We work with them to build a mixed programme of project activity that supports projects that remove emissions from the atmosphere and those that avoid further emissions.

This maintains flows of funding to develop and scale avoidance projects - from rainforest protection to clean cooking and safe water solutions,

Aqua Clara Water Purification Project, Kenya

Opportunities for project developers

Finance is available for high quality projects.

To access the finance available, you need to work with a partner who has a good understanding of and access to corporate demand.

Project owners are rightly focused on the business of delivering their project outcomes. Some need support to steer through the technical carbon asset development process to produce the type of high integrity carbon credits demanded by companies.

Other more established project developers may be interested in using carbon finance to scale their business further, for example to new regions or countries. We recommend working with an expert partner who has a proven track record of helping projects issue high quality credits and sell them over the lifetime of a project, and who will support you as the market fluctuates.

Methodologies already exist

There are existing methodologies to generate carbon credits for many project types including agroforestry, afforestation, reforestation, cookstoves, clean water access, bio energy, and sustainable land management. Other new methodologies, for example to cover some types of blue carbon projects, are in development.

If an appropriate project methodology doesn’t already exist, and you have a project activity which is demonstrably reducing emissions, there is the option to develop a new methodology and register it with the standards.

Rizome Bamboo Forestry, Phillipines

Climate Impact Partners has a long history of methodology development. We lead authored the first Gold Standard cookstove methodology in 2007, which allowed carbon finance for clean cooking projects and which is now used by more than 700 projects around the world. And we continue to innovate.

The recently approved Gold Standard methodology to measure carbon emission reductions from the use of electric and other metered cooking devices developed by Climate Impact Partners and the Modern Energy Cooking Services programme, will make a significant difference to the resources required for verifications.

With increasing demand, we’re going to see many more innovations such as the 14Trees project in Malawi where Climate Impact Partners worked closely with project partners to design a carbon project methodology that accurately calculates the carbon reductions achieved by using Durabric® rather than conventional kiln-fired brick alternatives.

In our experience the international approval process can often take up to two or three years, but it can open up access to carbon finance for new project categories. This is a complex but rewarding process and working with a partner who has experience and expertise in writing carbon methodologies and taking them through to approval is essential.

Post-COP27 Outcomes

New opportunities and new considerations for project development

One of the key outcomes of COP27 was greater clarity on the provisions of Article 6 and how nations can authorise mitigation outcomes for international transfer or for use in the VCM. However, there will be a period of uncertainty as new, Paris-era best practice is determined. COP27 has strengthened our view that the VCM will move towards multiple tracks – opening up new opportunities.

- Under Article 6 some carbon credits will be authorised for transfer of Emission Reduction units (ITMOs) between Parties through Corresponding Adjustments (CA) and some will not. Both will have a market but the authorization status will affect appropriate use of the credits.

- Countries will decide whether and how to encourage private sector investment within their national mitigation activities.

- Corporates will continue to support projects that resonate with their business and support their immediate, mid-term and long-term commitments - but how they communicate their actions will change.

To Sum It Up…

There is great opportunity for project developers to benefit from increasing corporate demand for both removal and avoidance projects to tackle climate change. However, accessing this demand and upfront development funding is not straightforward. Project developers looking to scale their impact will benefit from working with an experienced partner who has access to finance, is trusted by large, creditworthy buyers of credits, understands the complexity of carbon finance project development, and who is abreast of changes in the wider market that will influence their projects. Do that, and projects will be able to access and make best use of the opportunities which this unprecedented growth offers, and that means that together we can make real change possible.

- Ecosystem Marketplace, 2021, Ecosystem Marketplace's State of the Voluntary Carbon Markets 2021

- Voluntary carbon market 2022 in review webinar, link

- Voluntary Carbon Markets in 2023: A Bumpy Road Behind, Crossroads Ahead, link

- Climate Impact Partners, 2022, If not now, when? How companies are stepping up with the urgency required to deliver climate impact. View the latest annual research here link

Partagez cette page

$1 billion The amount of annual value the voluntary carbon market (VCM) is on track to exceed in 2021

Les toutes dernières Insights de

Climate Impact Partners

Reducing Scope 3 Aviation Emissions with SAFc: A Simple Starting Point

Sustainable Aviation Fuel certificates (SAFc) are emerging as a practical way to act today on Scope 3 emissions.

Pour en savoir plus

What does the SBTi's draft Corporate Net-Zero Standard 2.0 mean for carbon credit strategies?

Our experts Chris Duck and Hannah Blackmore unpack SBTi's draft Corporate Net-Zero Standard 2.0 and the role of carbon credits in long-term net-zero strategy.

Pour en savoir plus

Key Takeaways from UK Parliamentary Roundtable: Discussing the Future of Seagrass Restoration Investment

Key Takeaways from UK Parliamentary Roundtable: Discussing the Future of Seagrass Restoration Investment

Pour en savoir plus